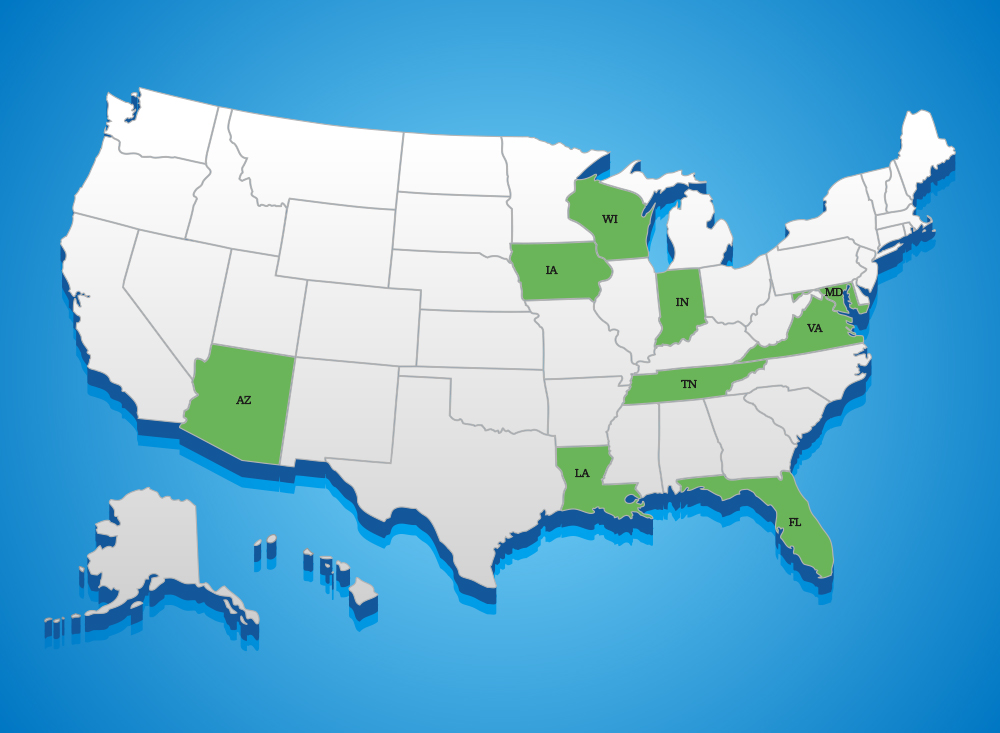

States enact dental benefit legislation

16 new laws passed in 9 states

Sixteen new dental benefit laws have been enacted in nine states, most of which have been supported by the ADA’s State Public Affairs program.

The states passed legislation addressing issues like assignment of benefits, claims review transparency, downcoding and bundling, medical loss ratios, prior authorization, provider network leasing, virtual credit card payments and insurer business practices review.

The eight states enacting dental insurance reform so far this year using SPA grants to support their campaigns are Indiana, Arizona, Tennessee, Virginia, Florida, Louisiana, Iowa and Maryland. Wisconsin did not apply for a grant in their successful insurance reform effort this year. The SPA Program was founded by the ADA in 2006 to help state societies manage specific public affairs issues and opportunities. It has since evolved into a national program which has helped state dental societies bolster their communications and public affairs capabilities.

Indiana

Indiana passed Senate Bill 132, which addresses two issues: assignment of benefits and provider network leasing. The new law requires insurers to comply with a patient’s request that the dental carrier send claim payments directly to the patient’s dentist regardless of the dentist’s participation status with the insurer. The new law gives dentists more control over insurer lease arrangements. It now ensures dentists can opt out of their contracted insurer’s network lease offer without negatively impacting the initial network contract relationship.

Arizona

Arizona passed House Bill 2444 which not only requires the state to publicize claim grievance information resolution statistics, it prohibits carriers from disallowing payments for covered services so long as patients consent to charges. Insurers’ disallow clauses that allow denials on claim payments and prohibit billing patients for dental services are now prohibited under the new law. Dentists are now free to work with their patients without insurer interference when services are not covered or if services are medically necessary and a claim payment is not made due to a denial or disallowance based on frequency. The state also passed Senate Bill 1070, which fortifies existing virtual credit card payments laws. The new law addresses concerns about insurers defaulting back to virtual credit cards after dentists opt-out by requiring insurers to abide by the provider’s decision on payment methods on a continual basis.

Tennessee

Tennessee addressed downcoding/bundling and virtual credit card issues in enacting House Bill 677. This law prohibits dental insurers from maintaining a plan that uses downcoding in a manner that prevents a provider from collecting the fee for actual services performed either from the dental benefit plan or the patient. It also prohibits bundling in a manner where a procedure code is labeled as nonbillable to the patient unless the procedure code is for a procedure that may be provided in conjunction with another procedure. Senate Bill 677 also addresses virtual credit card payments by preventing dental benefit plans from containing restrictions on methods of payment from the plan or its vendors to the dentist in which the only acceptable payment method is with a credit card.

Virginia

Virginia passed House Bill 1132, focusing on medical loss ratio and investigating insurer business practices. The law requires each dental carrier to annually report medical loss ratios to state insurance regulators. Additionally, it convenes a work group of stakeholders, including Virginia Dental Association representatives and dental carriers, to evaluate the need for changes regarding ethics and fairness in dental carrier business practices.

Florida

Florida enacted Senate Bill 892, which prohibits insurers from denying claims for procedures included in a prior authorization, barring extenuating circumstances like a patient exceeding annual maximum or the condition changing considerably since authorization. The new law also prohibits insurers from limiting claim payment methodology to credit card only. It requires dentists’ consent to electronic fund transfer claims payment protocols, and insurers may not require this consent on a patient-by-patient basis.

Louisiana

Senate Bill 463, enacted this year, provides transparency of patient premium expenditures for dental health care services. Leaning into the model adopted earlier this year by the National Council of Insurance Legislators, the law requires insurers to file a dental loss ratio report annually where the information is to be posted in a searchable format on the state’s department of insurance website. It sets reasonable limits on data that is included in calculating the dental loss ratio. Dental insurers also must provide the number of enrollees in their plans, the plan cost sharing figures, deductible amounts, annual maximum coverage limits, and the number of enrollees who meet or exceed the annual coverage limits.

Iowa

With the enactment of House File 2400, Iowa is leveling insurers’ control over practice operations with respect to virtual credit card payments and provider network leasing. The enacted bill requires insurers paying with virtual credit cards to notify the provider of any fees associated with each payment method, inform the provider of the available options for payment methods and provide clear instructions for the selection of an alternative payment method. It also requires that third parties leasing networks adhere to the provisions of the dentist’s original contract. Additionally, the contracting entity may not cancel, terminate or refuse to form a contractual relationship with a provider that chooses to not participate in that entity’s lease arrangements.

Maryland

Maryland establishes greater transparency and efficiency for patients using their dental insurance with the passage of Senate Bill 791. Among other things, it requires insurance carriers to provide contact information for each entity involved in their claims process along with detailed explanations for any coverage denials when requested. The new law strengthens requirements for grievances reviews under emergency situations. For non-emergency adverse decisions, the law requires explanation of the reasoning used to determine care was not medically necessary. It sets time limits on responses from insurers. Additionally, the law requires private review agents to attest to applying specific criteria in making decisions which include making decisions that are objective, based on peer-reviewed science, sufficiently flexible for deviations in care as needed and accountable for atypical diagnoses.

Wisconsin

Finally, Wisconsin’s Assembly Bill 62 requires insurers to pay a dentist directly, regardless of whether they are in-network, when the enrollee instructs the insurer to do so. While some insurers have refused to follow patient requests, this law ensures patients’ instruction on how their insurance product operates is followed by their insurer.

Insurance coverage for health care services is an important aspect of care delivery, the ADA said, but through careful analysis of the market and constant tracking of trends, the dental profession is identifying steady declines in value for patients and progressive increases in insurers’ efforts limit their financial exposure by reducing investments in care.

The ADA and state dental societies continue to advocate for the patients and dentists who care for them through laws that hold insurers accountable and reduce their influence on the dentist-patient relationship.

Follow all of the ADA’s advocacy efforts at ADA.org/Advocacy.